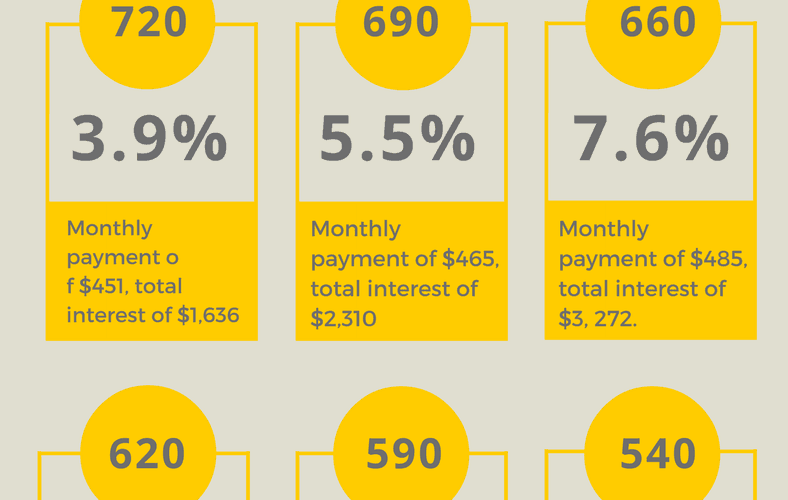

If you have a bad credit rating, you may think that financing a car is out of the question. The good news is that you can most definitely get a loan to buy a car with bad credit. The bad news is that you can bet your interest rate isn’t going to be good. If a lender is going to agree to extend credit to someone with negative credit history, they’re going to charge a higher interest rate in return for taking a chance on that person. Most people with credit scores below 600 pay around 15 to 17 percent interest on car loans. However, you shouldn’t let this fact deter you from getting a car if you need one.

The first step you should take before embarking on your car hunting adventure is to find out just how bad your credit is. You need to know the actual number so that the people in the finance office can’t make you believe it’s worse than it really is and try to stick you with an even higher interest rate or any other unnecessary additional charges. Go to MyFICO.com to find out the actual number. Anything under 600 means your credit is considered bad.

Once you know your credit score, you need to find out if you can get financing through a bank rather than through the car dealership. It may not be possible, but it’s much safer to buy a car this way. Car dealerships are known for shady practices. Their financing departments can’t be trusted. They want you to pay as much as possible for the car you are buying. A bank won’t try to add extra fees onto your loan, bully you into buying warranties, or have any say in how much to give you for your trade-in. They are an impartial third party. Places like Capital One Auto Finance are known for offering auto loans to people with less than perfect credit. If you aren’t able to get Capital One to extend credit, try AmeriCredit. If you already have the money in your hand when you go in to buy a car, the dealership is less likely to try to take advantage of you. When you don’t have the money and you are relying on them to extend the credit, there’s a bigger chance that you’ll get the wool pulled over your eyes.

If it’s clear that bank financing isn’t going to be an option, you’ll have to go through the dealership. This can be a successful experience if you keep a few things in mind. Even though you have bad credit, they don’t deserve to have the upper hand. It’s your money they want, and you have the power to walk away if they can’t offer you a deal you’re happy with. They definitely don’t want you to walk away. They want to sell you a car. Don’t be afraid to say no if you don’t like the deal they offer. Haggle with them. Tell them what you’re willing to settle for. In many cases, dealerships will negotiate with you even if you are a bad credit customer in order to move cars off the lot. Also remember that there are car lots out there that cater only to people with bad credit. Look for independently owned places that offer no down payment and weekly payment options without a credit check. You will definitely end up paying a lot more for a car than it’s worth if you go through a place like this, but if you need a car and have no other choice it’s an option for you.

After you’ve gotten your car, try to remember that refinancing later is a good idea. Work hard to repair your credit and keep up with what your score is. Once you’ve raised your score up to 600, you can start checking with other lenders to see if you can get a better interest rate on your vehicle. Making your car payments on time every month for at least a year will give banks and other lenders who wouldn’t work with you before more reason to trust you now.

<>