Buying a home is a huge step in the lives of many people, and it is a decision that is made with a great deal of care and consideration. Many people wish for the home of their dreams but worry about how to get a mortgage loan. There are many ways to obtain a mortgage loan to finance the home you’ve been dreaming of, it’s just a matter of persistence, strategy and knowledge.

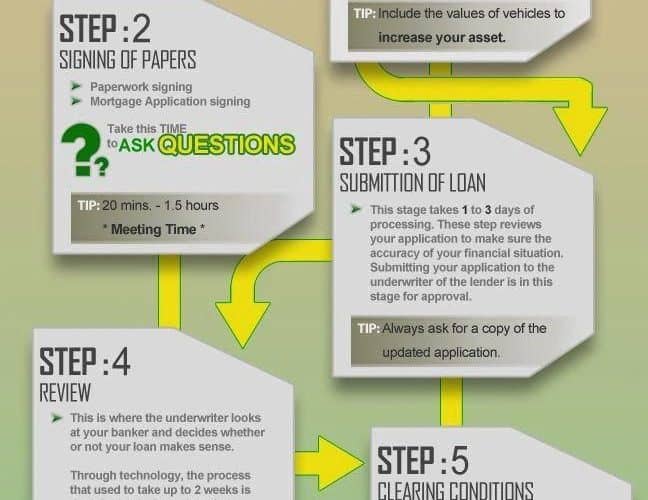

The first step in obtaining a mortgage loan is to analyze your current financial situation and compare it to the cost of the home you would like to purchase. This is often done by obtaining a copy of your credit report and analyzing your overall liabilities and assets. Many issues factor into getting the best rates for your mortgage loan, such as your overall debt, income and future earnings. Your credit score will be a major determinant factor, so it is important to know your score before starting to the process of obtaining a home loan.

For the first-time home buyer, there are many options available to assist you in your purchase. The most common type of loan for first-time buyers is the Federal Housing Administration or FHA loan. The loan requirements for FHA loans are generally more relaxed than other loan programs, and allow for more flexibility to assist in the purchase. FHA loans are structured to specifically assist buyers will low to moderate income, and allow the buyer to purchase with only a 3% down payment. This is far lower than most traditional loans that require a much higher down payment. FHA loans can be obtained from most banks and credit unions. In addition, FHA will work with other programs to assist you with the closing costs, and will allow you to obtain funds from relatives to make the down payment.

A second type of mortgage loan to consider is a conventional, fixed rate mortgage. Fixed rate mortgages are usually offered for 15 or 30 year terms, with the interest rate remaining steady over the entire life of the loan. In some areas, lenders will offer 40 or 50 year mortgages. This means that the loan payments will not change with fluctuations in the market, economy or other factors. This type of loan is best for the home buyer that expects a consistent income over the life of the loan and wants the mortgage payments to remain at the same level for the entire period of homeownership. Conventional home loans offer low rates to qualified buyers, however the lowest conventional rates are usually higher than those offered by FHA loans. In some cases, buyers with adverse credit histories may be required to pay higher interest rates, and pay as much as a 20% down payment on their mortgage loans.

Adjustable rate mortgages, or ARMs are mortgages that fluctuate over the life of the loan. The principle and interest payments may rise and fall, depending on market conditions. Many people choose these because they offer lower payments and rates at the outset. However, dips in the market can cause the mortgage payments to jump significantly, so this must be considered when choosing an ARM. Each lender has different terms when offering ARMs, so it is important to conduct thorough research and comparison shop when choosing this type of mortgage.

Obtaining a mortgage to finance your home purchase may seem intimidating and confusing. It doesn’t have to be. There are many programs on the market to assist a wide range of homebuyers, from first-time home buyers, to retirees looking for a second home. With the right amount of information, you’ll be enjoying your new home sooner than you think.

Related Posts

- How to Choose a Mortgage Lender?

- Credit Disputes to Affect 2012 FHA Mortgages

- Home Improvement Financing

- What are the Types of Homeowner Loans?