Closing is the second part of the two major steps in the home buying process.. The first part has to do with the signing of the contract in order to purchase the house. The closing part ensures that everything has been done and the house passes to the buyer in the condition specified in the contract.

To some it seems like a complicated process but it needn’t be so. It is just important to understand the main components in the closing process and have a good attorney by your side. Help on closing topics and finding an attorney can be found at realestatelawyers.com

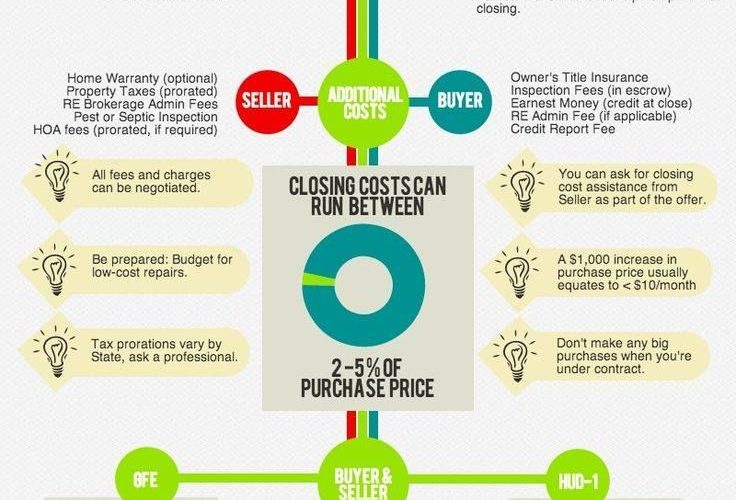

Closing costs can add up to 1- 4 percent of the total cost of the house. For example, if the house costs 300,000 dollars a buyer should expect to pay approximately three to twelve thousand dollars at closing. Mortgage-Investments.com has a closing costs calculator that can be used to help figure out closing costs.

At closing there will be numerous papers to sign during closing. Be ready to spend a few hours at the settlement company or the attorney’s office. It is important that the papers are read carefully and their should be an attorney there representing both the buyer and the seller’s interests.

The types of items included in closing include:

Property Insurance – which is required by the lender. The insurance is usually paid up for one year.

Property taxes – If the buyer is not paying all of the costs, both the seller and the buyer pay their share of the taxes for the time that each one has the house.

Home Warranties – will guarantee parts of the house such as appliances for a certain period of time

Recording Costs for Deed – This fee is for registering the new deed with the count Recorder of Deeds.

Brokers Commission – This cost is usually paid by the seller and takes care of the fee of the real estate agent

Certified Seals for Documents – These seals are required on various documents

Taxes required for the Transaction – As in other transaction where monies are paid for an item, government taxes apply

Costs for Attorneys – Attorneys are needed to make sure the proper papers are signed and to provide other legal service to the buyer and seller.

Title Company Costs – The title company will perform searches to make sure the title is clear and the seller is doing business with the rightful owner.

Survey Costs – These costs are required by the lender and confirms the house’s dimensions and assures land is not extending onto another property

Points – This is a pre-paid interest cost paid to the lender that will reduce the interest payments.

Appraisal Costs – attests to the house’s worth

Loan Application Costs – Buyer usually pays

Closing costs are paid by both seller and the buyer. In many instances a seller will offer to help with closing costs or to even pay the full amount as an incentive to sell the house. Sometimes the lender will wrap up the costs of closing within the loan. But to do so will probably add a fraction of a point to the interest rate.

Some closing costs can be deducted on the income tax statement. The costs that are able to be deducted are listed on the HUD-1 statement. On this statement is listed monies received and monies paid that has to do with the new house. Only those costs incurred that have to do with the sale of the house is deductible. For example a termite inspection is deductible but the cost of insurance cannot be deducted.